Here you will find BKF's recommendations for appointments at galleries.

Indicative terms for gallery agreements

Commission for the sale of works is agreed within a framework of 25-50 percent of the sale price.

Mediation of decoration tasks is agreed within a framework of 10-25 percent of the task's artist fee.

The gallery pays for the transport of artworks to and from the gallery.

The gallery covers the cost of insurance for works of art in the gallery's custody.

The gallery pays a separate fee to the artist for lectures, promotion, etc

If production costs, e.g. framing, materials, etc., amount to more than 5% of the sales price, the total production costs are deducted prior to distribution between artist and gallery.

To be able to use the advantageous artist VAT, sales through a gallery must take place as an instructional sale. This means, among other things, that the sale takes place on behalf of the artist and that the artist retains ownership of the work until payment to the gallery has taken place.

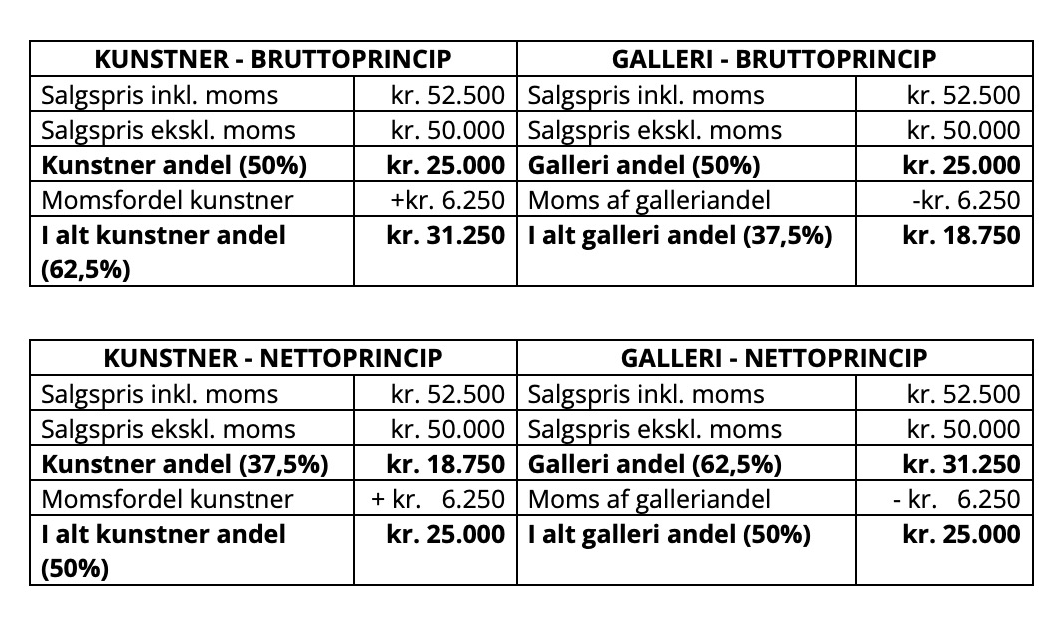

Settlement according to gross principle or net principle?

BKF believes that the profit from using the advantageous artist VAT should accrue to the artist and not the gallery. Therefore, BKF recommends that settlement between artist and gallery takes place on a gross basis.

If, for example, it has been agreed that the sale of works is distributed 50/50 between the artist and the gallery, the calculation looks like this according to the gross principle and the net principle respectively:

We use cookies to ensure that we give you the best possible experience of our website. If you continue to use this site, we will assume that you agree to it. We neither collect nor sell personal data to third parties.OKPrivacy Policy